BSE Code: 590051

CMP: 304

CMP: 304

It is into

information management (IM) and business intelligence (BI) services. Saksoft

has successfully transformed its business by acquired Acuma Solutions in 2006

and now recently took over Three sixty logica testing in 2014 which are into

testing and QA across various verticals of industry, customers and geographies.

It is now fully into data warehousing, business intelligence and data analytics….

It is focusing on mobile applications as well which is a big positive as there are only a few established and branded players in India in this segment.

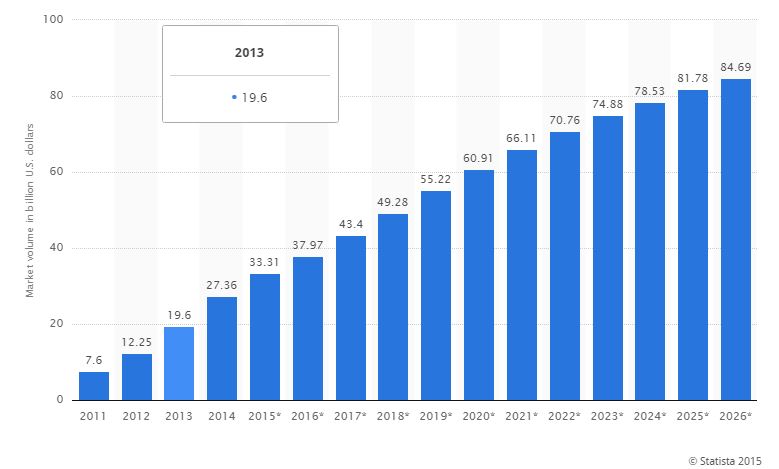

Big Data Growth Projections:

Big Data Growth Projections:

Saksoft

caters to banking, financial, travel & tourism, manufacturing, retail,

telecom. Logistics.. It was founded by Mr Aditya Krishna an ex citi bank

executive who was one of member of team which introduced citi bank credit cards

business in India successfully.

Revenue

Split up: 47% from UK, 38% from US, 14% from Rest of World.

Technology

partners: SAP, Tibco, Logi Analytics etc(all big names in data management)

EPS has

increased at the rate of 34% CAGR over 2011 to 2015

Debt to

Equity ratio decreased from .96 to .27 (company is reducing debt yoy)

Regular dividend

paying company..10%, 10%, 20%, 25%, 25% in fy10,fy11,fy12,fy13 and fy14

respectively.

Turnover

got more than doubled from 1050mn to 2315mn in 5 years…

EBIDTA

margin & NP grew at rate of 26% & 35% respectively since last 5 years

ROE in

double digit. Increasing yoy from 10% in fy10 to 15% in fy15

Despite of

investing 1000mn in aquisititions in recent past, Saksoft managed to reduce the

debt substantially…

It has

earned the loyality of customers as 50% of its customers are working with them

from last past 5 years continuously….

Total

headcount of 680 employees across UK,US, India and Singapore

Risks which

can come at anytime in an IT Company

Compliance:

Saksoft major chunk of revenue comes from US and UK and it has not sensored by

any customer in these countries. It gives confidence that company is taking all

measures to mitigate the compliance related risks

Big Data is

driving the profitability of most of micro and midcap IT Companies since last 2

years and this business segment is poised to give exponential profits to organizations

who are fully into it. In last 2 years there were couple of companies who are

into big data, the stock prices of them gave 2000% returns. Saksoft is still

undiscovered. Promoter shareholder is very good and most of open stocks are in

strong hands. Liquidity is very less. There is no FII and DII holdings which is

a big positive.

Recently stock prices has witnessed a sharp jump upwards(including many upper circuits), but i think there is a lot of more to come.

Next 2

years would be game changing for this organization which is sailing on big-data and mobile applications business model.

It is just

an analysis and not a recommendation to buy this stock. Please do full due

diligence before buy it.